Net Working Capital is a concept that arises in most M&A transactions involving the sale of an ongoing California business by the owner or seller to a buyer. If the transaction is purely for the business’s hard assets, Net Working Capital would not be part of the conversation or the transaction.

Think of Net Operating Working Capital as the fuel already in the engine; it is what allows the car to idle and move forward right now. Strategic Working Capital is the fuel in the gas tank; it determines how far the car can actually travel. It also decides whether it has enough power to climb a steep hill or reach a new destination.

Learn more about business valuation.

Download a sample business valuation report.

Key Takeaways:

Operational Necessity vs. Asset Sales

Net Working Capital (NWC) is a fundamental concept in M&A transactions involving the sale of an ongoing business. It is entirely excluded from transactions that involve only hard assets. In an ongoing business, NWC represents the difference between current assets (such as accounts receivable and inventory) and current liabilities (such as accounts payable and accrued expenses) required to sustain daily operations.

The “Peg” and Price Adjustments

Buyers and sellers negotiate an NWC “Peg” or Target. The “Peg” or “Target” acts as a normalized benchmark typically calculated using a trailing twelve-month (TTM) average to smooth out seasonal fluctuations. The final purchase price is subject to a post-closing “true-up,” where the price is adjusted dollar-for-dollar based on whether the actual NWC delivered at closing is above or below the agreed-upon Target.

Operating vs. Strategic Capital

There is a critical distinction between Net Operating Working Capital (NOWC), NOWC includes the immediate assets like Accounts Receivable and Inventory needed to generate the revenue used to value the business. Strategic Working Capital includes Cash, Credit Lines, and Growth Capital. NOWC is the “fuel in the engine” that keeps the car idling. Strategic Working Capital is the “fuel in the tank” that a buyer needs to ensure the business remains strong and continues to grow after the sale closes.

Analysis of Operational Drivers

A comprehensive NWC analysis requires moving beyond simple formulas to examine detailed month-to-month spreadsheets that account for seasonality, vendor payment terms, and employee bonus cycles. Disputes often arise when the Target NWC is based on historical management financials. Still, the Closing NWC must be prepared strictly in accordance with Generally Accepted Accounting Principles (GAAP) or the specific bespoke rules in the purchase agreement.

Exclusions and Specialized Items

Most M&A deals are conducted on a “cash-free, debt-free” basis, meaning cash and interest-bearing debt are typically excluded from NWC and handled separately in the funds flow. Deferred revenue—cash collected for services not yet performed—is a highly negotiated item; it may be treated as debt, included in the NWC mechanism, or handled via a “cost to serve” model, in which the seller leaves behind enough cash to fulfill future obligations.

Andrew’s take:

Think of NWC as the tide in a harbor. The Purchase Price is the value of the ship itself. The Target NWC (The Peg) is the agreed-upon water level needed for the ship to float and sail out to sea. If the tide is higher than the Peg at the moment of the hand-off (Actual NWC), the seller has provided extra “water” and earns a higher price; if the tide is lower, the buyer is getting a ship stuck in the mud and must be compensated for the cost of dredging it out.

Prefer to watch a video? Hit play and watch below!

What is Net Working Capital?

At a basic level, Net Working Capital is typically explained by looking at a business’s Balance Sheet and subtracting Liabilities from Assets, or “Assets – Liabilities.”

However, as I came to learn at a conference I attended with the M&A Source (www.masource.org) in Phoenix, AZ and listening to a presentation by Mr. Monty Walker and two of his cohorts, there is much more to the question – what is Net Working Capital?

Seeing that the presentation was given in the context of a boxing match, I’ll use this theme in this article.

The boxing match Referee and the two Boxers

By way of introduction, Monty is a CPA and is based in Texas. Here is a link to Monty’s website: www.walkeradvisory.com

Does Monty know what he’s talking about? You bet! He was invited to testify before the US Congress about the implications of taxes on privately held businesses and accepted the invitation. Plus, if you check out Monty’s website, you’ll see lots of information about taxes and related matters you’d like to know. This is especially true if you own a Privately Held business or plan to own one.

Staying with the boxing theme and Monty’s CPA training, Monty loves analyzing the balance sheet for various purposes, including Net Working Capital. When the seller, buyer, and their advisors are arguing over the numbers, Monty loves to referee. He ensures a fair outcome for both parties. That is, Monty loves to pull no punches.

This was the role Monty played when two gentlemen decided to put on the gloves. They threw some punches to knock out their opponent in an argument over Net Working Capital. Neither was successful, but let’s join them in the ring to see what played out.

The two cohorts to join Monty ‘Referee’ Walker in the ring were Bob ‘Take no Prisoners’ McCormack and Scott ‘Powder Puff’ Mashuda. Bob and Scott are, by profession, Investment Bankers and love helping entrepreneurs get the financing they need to close a deal.

You can learn more about Bob at his website or https://murphymccormack.com. You can learn more about Scott from his website or https://reag.com. Warning! Don’t ask Scott why he’s called ‘Powder Puff’.

Is your business currently operating at the top of its game? Send a free inquiry today!

Call Andrew Rogerson, Rogerson Business Services, toll-free (844) 414-9700 | Leave a message – I’ll call you right back

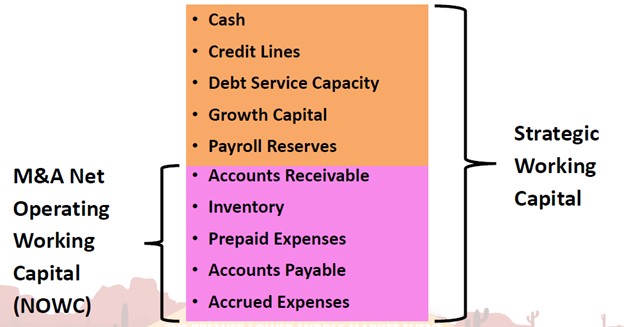

What is Net Operating Working Capital (NWOC) and Strategic Working Capital?

Earlier, we said Net Working Capital was Assets minus Liabilities or ‘Assets – Liabilities.’

However, once you get into a transaction, it typically becomes more complex and sophisticated as the concepts move to Net Operating Working Capital and Strategic Working Capital.

To present it simply:

Net Working Operating Capital is:

- Accounts Receivable

- Inventory

- Prepaid Expenses

- Accounts Payable

- Accrued Expenses

Strategic Working Capital is:

- Net Working Capital as defined above.

- Cash

- Credit Lines

- Debt Service Capacity

- Growth Capital

- Payroll Services

NOWC V Strategic Working Capital

Monty likes to present this simple analogy.

- Net Operating Working Capital is the fuel already in the engine.

- Strategic Working Capital is the fuel in the tank.

If there is fuel in the engine but little to no fuel in the tank, the car won’t go very far.

So, if a buyer purchases the business with only fuel in the engine but wants their business to stay strong and grow, additional Working Capital is necessary. Either the buyer needs to have it in savings to add to the Balance Sheet, or they borrow it as additional Working Capital.

What amount of Working Capital should the buyer receive when they buy a business?

According to ‘Referee’ Walker, Operating Working Capital should be an amount sufficient for the business to generate the same amount of gross revenue and earnings used in determining the purchase price.

Is that the correct answer?

Well, it depends on whether you are the Seller, the Buyer, or the Lender.

Is there anything else to consider?

You bet!

Here are a few items to consider as you dance around the boxing ring.

What about the cash-on-hand policy of the business?

If the business offers terms to its customers, it has money sitting in Accounts Receivable.

- What is the policy of the business for how many days the business should have?

- What if a large customer is given a longer time to pay their AR?

- What are the terms of paying vendors?

- What is the policy on inventory if the business carries inventory?

What about seasonality?

An important variable to consider is whether the business has seasons.

Seasons can include periods when the business is quiet and others when it is busy.

Examples include:

- Is the business busier or quieter leading up to Christmas?

- Is the business busier or quieter if the weather is extreme?

- Is the business busier or quieter during school holidays?

- Does the business have a major customer or two that buy at certain times of the year?

- Does the business pay employee bonuses, and when are they paid?

- Does the business owner prefer to put cash or a bonus in their pocket at certain times of the year?

- Are there any prepaid services the business uses that must be paid in full each year, and how does that affect the business’s cash flow?

A simple method to analyze this information is to look at a month-to-month Profit and Loss Statement, and for the buyer to ask questions.

What about an Earnout?

What if the seller agrees to accept an Earnout from the buyer?

Is the Earnout paid monthly, quarterly, half-yearly or annually, and are funds being set aside to cover this expense?

What about a customer concentration?

- What about one customer that makes up 25% or more of the annual Gross Revenue?

- Do contingencies need to be considered when the business has a change of ownership?

Let us negotiate as Artificial Intelligence cannot help you.

A final thought, and it’s about Artificial Intelligence (AI).

There is currently a lot of hype around Artificial Intelligence (AI) and what salespeople say it can and cannot do. Therefore, if it’s suggested that AI can help, be careful. If AI uses a report or series of reports to provide solutions, then whatever reports AI provides will be wrong. As the saying goes – Garbage In and Garbage Out.

A better approach is to ask questions in different ways.

Net Working Capital, Net Operating Working Capital, and Strategic Working Capital are concepts. These concepts require building detailed spreadsheets. Once a spreadsheet is built, it requires analysis and questioning to make and implement decisions.

The table below explains key working capital components and concepts:

Capital Concept |

Formula or Calculation |

Core Components |

Primary Objective |

Engine Analogy |

Key Influencing Factors |

Net Operating Working Capital (NOWC) |

$(AR + Inventory + Prepaids) – (AP + Accrued Expenses)$ | Accounts Receivable, Inventory, Prepaid Expenses, Accounts Payable, Accrued Expenses | Maintain the specific revenue and earnings levels used to determine the purchase price. | Fuel already in the engine (allows the vehicle to idle or move immediately). |

Seasonality (holidays, weather), business policies (payment/collection terms), and cash flow timing.

|

Strategic Working Capital |

$NOWC + Cash + Credit Lines + Debt Capacity + Growth Capital + Payroll Services$ | NOWC components, Cash, Credit Lines, Debt Service Capacity, Growth Capital, Payroll Services | Ensure long-term health and provide resources for expansion and future growth. | Fuel in the tank (determines how far the vehicle can travel or climb). |

Capital structure, ability to assume new debt, and specific growth initiatives.

|

Net Working Capital (Academic) |

$Current Assets – Current Liabilities$ | Current Assets, Current Liabilities |

Provide a general assessment of the financial position of a business.

|

||

Hard Assets |

Valued based on physical condition and market worth | Equipment, real estate, machinery (e.g., ovens), display cases, buildings | Acquisition of physical components rather than the operational cycle. | The static tools (the ovens) without the momentum (the flour or dough). |

Physical condition and market worth; typically static and unaffected by seasonality.

|

Buying a business is like buying a car to start a delivery service. The purchase price gets you the vehicle itself. The Net Working Capital is the gas already in the tank. If you arrive and the tank is empty (NWC is below target), you have to spend your own money just to drive it off the lot, so the seller owes you a discount. If the tank is completely full (NWC is above target), you’re getting extra value you didn’t pay for, so you owe the seller for that extra fuel.

Andrew Rogerson’s Value Proposition

With over 20 years of experience in the California M&A market, Andrew Rogerson and his team at Rogerson Business Services offer expert guidance and support to business owners seeking to sell their companies. Their services include:

- Business Valuation: Accurate and comprehensive valuation assessments using a combination of methodologies.

- Marketing for Sellers to find qualified and motivated buyers: Targeted marketing campaigns to reach qualified buyers and generate interest.

- Negotiation and Deal Structuring: Skilled negotiation and deal structuring to achieve optimal outcomes that are a win for the seller and the buyer.

- Due Diligence and Closing Support: Assistance with due diligence, legal documentation, and closing procedures, including escrow services.

- Confidentiality and Discretion: Maintaining strict confidentiality throughout the sale process.

By partnering with Rogerson Business Services, you can leverage their expertise and network to achieve a successful sale and maximize the value of your business in California, which is valued between $1 million and $50 million. Get Free Consultation.

Got burning questions? Send Free Inquiry Today.

Frequently Asked Questions

How does Net Working Capital in M&A differ from the standard accounting definition?

While the simple academic definition of working capital is current assets minus current liabilities, the M&A definition is more refined. In most transactions, businesses are sold on a “cash-free, debt-free” basis, meaning the seller keeps the cash and settles all interest-bearing debt. Therefore, M&A Net Working Capital typically excludes cash, cash equivalents, and both short-term and long-term debt. The focus is purely on the operational assets and liabilities (such as accounts receivable, inventory, and accounts payable) required to sustain the company’s daily revenue-generating activities.

What is an NWC “Peg” and how is it calculated?

The “Peg” or NWC Target is a negotiated, normalized amount of working capital that the seller is expected to deliver to the buyer at closing. It serves as a benchmark to ensure the buyer has sufficient liquidity to run the business without an immediate cash infusion. The most common method for determining the Peg is calculating the average monthly NWC over the trailing twelve-month (TTM) period. This 12-month lookback is used to smooth out seasonality, business cycles, and one-off events.

How does the NWC adjustment affect the final purchase price?

In almost all M&A deals, the purchase price is subject to a post-closing “true-up” mechanism. This adjustment is usually dollar-for-dollar based on the difference between the Actual NWC delivered at closing and the agreed-upon Target NWC.

- Actual NWC > Target: The buyer pays the seller the difference, which increases the purchase price.

- Actual NWC < Target: The purchase price is reduced, and the seller effectively reimburses the buyer for the shortfall.

What are “debt-like items,” and why are they excluded from NWC?

Debt-like items are liabilities that may not be traditional bank debt but represent future cash outflows for obligations incurred by the seller. Because these items are often non-operational or relate to the seller’s period of ownership, buyers prefer to treat them as indebtedness (deducted directly from the purchase price) rather than including them in the NWC calculation. Common examples include:

- Accrued bonuses or commissions resulting from management decisions made before the sale.

- Unfunded pension obligations or earned but unpaid PTO.

- Legal settlements or professional fees related to the transaction.

Why is the treatment of deferred revenue so contentious?

Deferred revenue represents cash collected by the seller for services yet to be performed. In a cash-free, debt-free deal, the seller walks away with the cash, but the buyer inherits the obligation to provide the service. Buyers argue it should be treated as debt because they must expend resources to fulfill the contract without receiving additional cash. Sellers argue it is a regular part of the working capital cycle and should be part of the NWC Target. A common compromise is the “cost to serve” model, in which the seller retains enough cash to cover the actual costs of servicing post-closing obligations.