By Andrew Rogerson, Founder, Rogerson Business Services (California M&A advisory) When considering an Environmental M&A Advisor vs. a Generic Broker, it’s important to understand the differences between these roles in the context of business acquisitions.

Last updated: March 5, 2026

Author note: This guide reflects common SMB sell-side practice in California environmental services transactions. It is not legal, tax, or investment advice.

Sources and methodology: I cite primary regulators (e.g., South Coast AQMD, California Water Boards, DTSC) for permit-transfer and compliance process basics. Additionally, I use market studies and sector research (e.g., SRS Acquiom deal-terms summaries, ABA M&A Committee materials, and investment bank sector updates) to describe typical deal terms and buyer behavior. Because terms vary by deal size, risk profile, and market conditions, I describe patterns and caveats rather than guarantees.

Thinking about selling an environmental services company in California? As of 2026, the stakes feel higher: tighter permitting rules, heavier diligence, buyer scrutiny of successor liability, and credit conditions that reward prepared sellers. This guide compares an industry-specialized environmental M&A advisor with a generic business broker. It will help you choose the right partner. Primary keyword: environmental business brokers California.

Testimonials

Valerie M. Bruns

“In the last few months I have read or scanned a number of books on selling a business and have to say yours was by far the best.

I’m fairly familiar with the nuances of selling a business, but your book is at the head of the herd because it’s not only informative, but it walks a prospective seller thru the actual steps from formulating the decision to sell, researching prospective buyers, due diligence to closing.“

Valerie M. Bruns – Dundee, IL

See more reviews and testimonials.

Is your business currently operating at the top of its game? Send a free inquiry today! Call Andrew Rogerson, Rogerson Business Services, toll-free (844) 414-9700 | Leave a message – I’ll call you right back

Key takeaways

- Choose a specialist for regulated subsectors—hazardous waste transport, remediation, environmental testing labs, water/wastewater O&M, and industrial hygiene—because they navigate permits and liability structures with fewer surprises.

- Expect tighter liability structuring in California: asset vs. stock decisions, indemnities, escrows/holdbacks, and selective use of RWI; specialists coordinate the playbook with counsel and insurers.

- Depth of buyer coverage matters; specialists maintain PE/strategic shortlists specific to environmental niches and prewire financing paths to raise cash at close and reduce contingencies.

- Strong preparation reduces fall-through: specialists often assemble QoE, permit-transfer plans, and environmental diligence packs pre-LOI, which can help shorten timelines and reduce re-trades.

- A reputable generalist can be a good fit for simpler, sub-$1M EBITDA businesses when process overhead would outweigh the advantages of specialists.

Prefer to watch a video?

Hit play and watch below!

If you operate in a regulated environmental niche or need maximum certainty and cash at close, hire a specialized M&A advisor. If your business is smaller and straightforward, a strong generalist broker can work—provided they accept a disciplined, NDA-gated process. They must also coordinate early with California counsel on permits and successor liability.

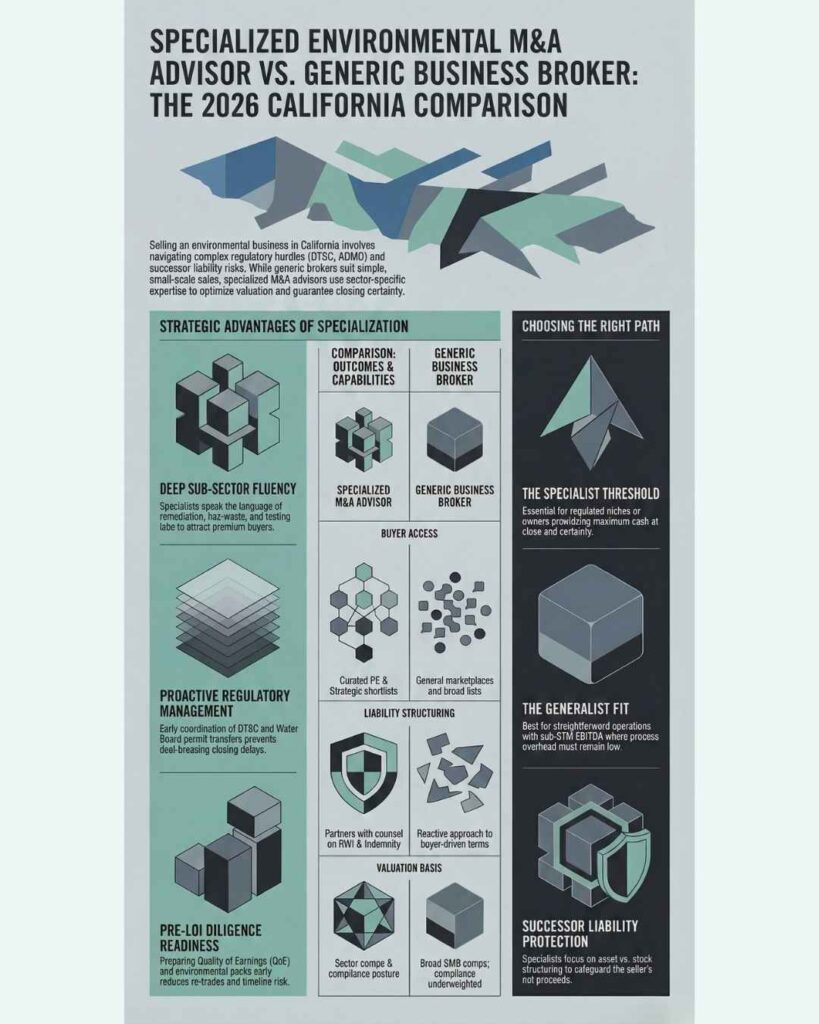

Environmental business brokers California: side-by-side comparison

Below is a practitioner-oriented snapshot of how outcomes typically differ in California environmental deals (as of 2026). Claims reflect common market practice; verify specifics with your counsel/CPA.

Dimension |

Specialized environmental M&A advisor (California-focused) |

Generic business broker (non-specialized) |

Sub-sector fit |

Deep coverage in remediation, haz-waste transport, testing labs, water/wastewater O&M, and industrial hygiene; speaks the language buyers expect. | Broad small-business coverage; less fluency in regulated environmental niches. |

Buyer access & network depth |

Curates PE platforms and strategic acquirers active in environmental services; runs targeted, NDA-gated outreach. | Relies on general buyer lists and marketplaces; sector-fit vetting varies. |

| Valuation signals & comps | Uses sector comps, contract quality, compliance posture, and permit transfer risk to frame price; positions for premium where justified. | Leans on broad SMB comps; environmental compliance and permit risk are often underweighted. |

Diligence readiness |

Coordinates QoE, Phase I/II ESA context, and permit-transfer plans pre-LOI to reduce re-trades and fall-through. | Provides basic marketing materials; diligence prep often deferred to post-LOI, increasing timeline risk. |

CA liability structuring |

Partners with counsel on asset vs. stock, indemnities, escrows/holdbacks, and RWI suitability; aims to mitigate successor liability. | Follows buyer/counsel lead; less proactive on indemnity and RWI design for environmental exposures. |

Time-to-close & certainty |

Tighter process control, prewired lenders, and prepared diligence frequently compress LOI→close. | More variability; surprises in permits/financials can trigger extensions or broken LOIs. |

Confidentiality & process control |

Enforces strict NDA gating and controlled communications to protect employees and customers. | Mixed rigor; broader marketing can raise leak risk. |

Buyer credentialing & financing |

Screens for sector fit, proof of funds, and lending appetite; aligns financing early. | Screening depth varies; financing readiness often surfaces later in the process. |

Regulatory/permit transfer |

Anticipates DTSC/SWRCB/AQMD/ELAP steps; sequences filings and closing conditions with counsel. | Addresses permit reactively; transfer requirements can delay closing. |

Post-close claims & disputes |

Negotiates market-aligned caps/survival and targeted escrows; considers RWI where feasible. | Terms are often buyer-driven; broader escrows or longer survival can creep in. |

Fees & alignment |

Retainer plus success fee; higher prep intensity, lower commission percentage at higher EV bands. | Higher commission on smaller deals, minimal upfront prep; lower fixed costs early. |

Best for |

Regulated subsectors; sellers prioritizing certainty, valuation optimization, and cash at close. | Simple businesses, sub-$1M EBITDA, or owners prioritizing speed over optimization. |

How to choose your subsector and goals

Use this quick decision path to narrow your fit.

- Operate in a regulated niche or hold sensitive permits (DTSC hazardous waste, Water Board NPDES, South Coast AQMD)? Choose a specialist to pre-plan transfers and structure liability.

- Want maximum cash at close with minimal rollover or earnout? Choose a specialist who can run a competitive, lender-prepped auction.

- Need QoE cleanup or have data gaps? Choose a specialist to coordinate accountants, environmental consultants, and a tight VDR.

- Is confidentiality paramount with employees/customers? Choose a specialist for strict NDA-gated outreach.

- Under ~$1M EBITDA with straightforward operations? A reputable generalist can suffice if they agree to a measured, permit-aware process.

Is your business currently operating at the top of its game? Send a free inquiry today! Call Andrew Rogerson, Rogerson Business Services, toll-free (844) 414-9700 | Leave a message – I’ll call you right back

Why specialists often achieve better outcomes in California

Permits and regulatory transfers drive the deal calendar

California agencies require specific steps to change ownership or operator status. For example, South Coast AQMD details change-of-owner/operator procedures, forms, and timelines in its December 2024 guidance; sellers should expect fees and defined review paths according to the district’s rules. See the agency’s official Change of Owner/Operator Guidelines for process specifics in its jurisdiction, anchored by the published rules governing permit transfers or voids when ownership changes, including Rule 209, Transfer and Voiding of Permits. Authoritative details appear in the district’s program documents: South Coast AQMD change-of-owner/operator guidelines (2024) and South Coast AQMD Rule 209.

Statewide, NPDES and other discharge permits issued by the State Water Resources Control Board and regional boards require pre-transfer coordination; permits are not automatically assignable in many cases. Review the program hub for transfer expectations and coordinator contacts in your region per the board’s NPDES Program portal: California Water Boards NPDES Program.

For hazardous waste facilities or operations regulated by DTSC, ownership or operator changes generally require prior approval and application updates under the state’s RCRA-aligned framework; start early with the department’s permitting contacts and facility tracker for status context: DTSC program portal.

Specialized advisors anticipate these hurdles, choreograph filings, and write closing conditions to avoid permit gaps—one of the biggest sources of delay and valuation erosion in environmental deals.

Liability structuring protects your net proceeds.

In California environmental transactions, deal structure does the heavy lifting. Specialists work with counsel to prefer asset deals when successor liability is a key concern, or to price and insure stock deals when buyer objectives demand entity continuity. They negotiate indemnity caps and survival periods that align with prevailing private-target norms, reserve targeted escrows for known issues, and consider reps & warranties insurance (RWI) when feasible.

Market studies indicate how terms evolve year to year. SRS Acquiom’s recent private-target deal terms summaries (2019–2024 data, published 2025) describe shifting survival periods, special escrows, and claim activity that sellers should factor into negotiations; see the firm’s overview articles for directional benchmarks in today’s market per the 2025 trends analysis: SRS Acquiom’s deal terms insights. For a deeper legal baseline on indemnity caps, baskets, and survival norms in private deals, consult the ABA’s M&A Committee materials and its widely cited Private Target Deal Points Study (membership/purchase required): American Bar Association — M&A Committee.

Because permitting and compliance histories differ widely across environmental companies, a specialist will tailor indemnities for site-specific risks, negotiate specific environmental escrows when needed, and coordinate any agency-required undertakings into the purchase agreement and closing checklist.

Buyer access and financing pathways raise price and certainty.

A specialist’s rolodex skews toward PE platforms and strategics already active in environmental services. Those buyers pay for proven compliance programs, recurring municipal/utility contracts, and accredited lab capabilities. Sector updates from investment banks covering industrial and environmental services highlight consistent buyer interest and premium pricing where compliance infrastructure is strong; see this recent review for context on buyer activity and premium drivers in the space:

On financing, specialists prewire lenders and equity sponsors. Hence, shortlisted buyers arrive with indicative terms and fewer contingencies, which can translate into more cash at close and tighter certainty when you sign an LOI.

Case study: Environmental testing lab sale (representative, California)

Situation: A California environmental testing laboratory with ELAP accreditation sought an exit at a premium valuation. The owners ran lean finance functions and needed QoE cleanup to normalize EBITDA and address working-capital seasonality. Accreditation continuity and method compliance documentation were mission-critical to buyers.

Strategy: The sell-side team positioned the business for an asset sale to mitigate concerns about successor liability while preserving accreditation continuity. Before outreach, the team coordinated third-party QoE, assembled evidence of method compliance, documented instrument maintenance/calibration, and drafted a permit and accreditation transition plan. Later, outreach targeted a shortlist of PE-backed platforms and strategic consolidators in the testing and compliance services space. All parties executed NDAs before accessing the data room.

Process and timeline: Buyers received a clear calendar—management meetings after initial IOIs, followed by confirmatory diligence under a staged request list. The team sequenced agency communications so that ELAP and local air district notices aligned with closing conditions. The buyer and lenders reviewed QoE and operational diligence early. As a result, they compressed confirmatory work after the LOI.

Outcome pattern (representative, not a guarantee): The parties agreed to an asset purchase agreement with market-aligned indemnity caps and survival, a targeted specific-issue escrow, and a working-capital true-up. Because diligent preparation reduced surprises, the closing timeline tracked closer to the faster end of the typical lower-middle-market range.

Note: Accreditation and permit-transfer rules can change; coordinate directly with program administrators (e.g., ELAP and your regional air district) early in the sale process.

Fees, alignment, and net proceeds

Specialists often charge a modest retainer plus a success fee that steps down by enterprise value tiers; in exchange, they invest early in valuation work, the CIM, buyer mapping, and a secure data room. Generalists commonly rely on a higher commission for smaller deals with minimal upfront preparation. Either model can work; the question is whether the process intensity matches your risk profile and deal size.

Your net after-tax proceeds depend on more than commissions. Escrows, survival periods, earnouts, rollover equity, working-capital adjustments, and state taxes all move the final number. For a refresher on structure mechanics, see this explainer on asset-versus-stock sale dynamics in California: asset vs. stock sale comparison (California overview). If you anticipate an asset sale, review common sales-tax considerations for transfers of business assets here: California sales tax on business asset sales — overview. Owners also model state taxes on gains; for planning context, see this primer on how California treats business capital gains at individual rates: California capital gains tax basics for business sellers.

Is your business currently operating at the top of its game? Send a free inquiry today! Call Andrew Rogerson, Rogerson Business Services, toll-free (844) 414-9700 | Leave a message – I’ll call you right back

FAQ — California-specific questions sellers ask

What is the difference between an asset sale and a stock sale for environmental businesses?

Think of an asset sale as picking the pieces to transfer; a stock sale transfers the whole entity. In California environmental deals, asset sales can help mitigate successor liability, but they can trigger new or transferred permits and potential sales-tax considerations. Review the mechanics in this educational overview: asset vs. stock sale comparison (California overview) and discuss the fit with counsel.

Can RWI cover environmental liabilities in lower-middle-market deals?

RWI can backstop general reps; insurers often exclude known environmental issues and site conditions or price them separately. A specialist will judge when RWI is worth pursuing, given deal size and exposure profile. The specialist will use prevailing private-target terms for caps and survival as a baseline; see directional trends here: SRS Acquiom’s deal terms insights and the ABA’s M&A Committee materials: ABA — M&A Committee.

How long does it take to sell an environmental testing lab in California?

Timelines vary with preparation, buyer type, and permit steps. When sellers prepare QoE and a permit/accreditation plan pre-LOI, specialists often compress the LOI-to-close window relative to less-prepared processes. Expect meaningful gating items around air district change-of-owner filings and accreditation continuity.

Do I owe California sales tax when I sell business assets?

California’s tax agency provides the baseline rules and bulk-sales guidance. Whether tax applies depends on what you sell and how you structure the transaction, so confirm with your CPA before you sign an LOI. See the California Department of Tax and Fee Administration’s bulk sales overview and related notices: CDTFA — Bulk Sales.

Which permits commonly require action when ownership changes?

Air permits in the South Coast AQMD jurisdiction, NPDES and other discharge permits under the Water Boards, and hazardous waste permissions overseen by DTSC often require prior filings or approvals. Start with these official program pages: South Coast AQMD change-of-owner/operator guidelines (2024), California Water Boards NPDES Program, and DTSC program portal.

Next steps and resources

- Map your permits and contracts, identify required consents, and draft a pre-LOI diligence plan with your advisors.

- Interview intermediaries using a sector-specific scorecard (buyer coverage, diligence plan, permit-transfer strategy, liability structuring experience, lender relationships).

- Build a proceeds model that tests escrow sizes, earnouts, rollover, and tax assumptions before you set valuation expectations.

For deeper learning, explore this educational library on California M&A concepts and planning checklists: M&A knowledge hub for California business owners.

Is your business currently operating at the top of its game? Send a free inquiry today! Call Andrew Rogerson, Rogerson Business Services, toll-free (844) 414-9700 | Leave a message – I’ll call you right back

Disclaimer: This article is for informational purposes only and reflects practices and sources available as of 2026. It is not legal, tax, or investment advice. Always consult licensed California counsel and a CPA before making decisions.